How to create a personal financial plan and what is it? Personal financial plan (LPP)- this is a forecast of income and expenses of the family budget for the long term. Like any plan, physical therapy allows you to achieve any goals.

This could be: paying off all debts, saving for a major purchase: a vacation trip, a car, a summer house, apartment renovations, etc., or creating a family reserve fund for a rainy day, investing in financial instruments, and so on. Before you make any major financial decision, make a plan.

A personal financial plan is a course that allows you to correctly move towards your intended goal, but it can be adjusted taking into account changes that have occurred in the family’s financial flows.

The effectiveness of the plan depends on its duration - the longer the period, for example, 5-10 years, the higher the result will be from it than from a plan drawn up for several months. True, the longer the period, the more difficult it is to make forecasts; for starters, you can try to make a plan for 6 months - 1 year.

Always leave a certain amount as a reserve for unexpected expenses - this is the financial security of your family.

Accounting for income and expenses

In order to create a personal financial plan, experts advise starting to track your income and expenses. And only after 2-3 months of accounting, compile a physical form. I believe that one month will be sufficient to determine the correct statistics of the family budget.

With income, everything is simple, usually it is a small list - wages, bonuses, scholarships, pensions, child benefits, income from rental real estate, and so on. Income is easy and pleasant to track, but expenses are more difficult.

If monthly expenses are of the same type, they can be identified by elimination. For example, calculate the amounts for utilities (rent for housing), kindergarten, Internet, mobile communications, loan payments, travel. These amounts are repeated from month to month.

If there are no other expenses (entertainment, recreation, clothing, etc.), then everything else is food and household chemicals. The main thing is to be honest with yourself when accounting for expenses and not reduce them. If you spent half your salary on a handbag, cosmetics or computer games, honestly reflect this in your accounting.

So, we sorted out the income and expenses. If you can break down your monthly budget into items and clearly define the amounts for them, then you can move on to the next step.

Goals

You need to define and clearly formulate goals for the period for which you will draw up a plan. For example, pay off your mortgage loan as quickly as possible and save money on interest, and invest the money that previously went to the bank.

Or save money for your dream car, a cool computer or a vacation in the Canary Islands. There will most likely be several goals: both large and small, here you need to decide what is priority and in what sequence to complete them.

The plan will help you find out how achievable your financial goals are and how long it will take to achieve the goal. If your goals are unattainable, for example, buying an apartment, you need to think about a loan or give it up for a while until your financial situation improves. When drawing up a plan, the interests of the whole family must be taken into account.

How to draw up a personal financial plan: an example of a personal financial plan

For an example of drawing up a plan, take the following data:

Family of 4, with two minor children. A husband and wife together earn 100,000 rubles a month. They purchased an apartment with a mortgage, the monthly payment is 25,000 rubles. For the purchase of an apartment, the spouse receives a property deduction for personal income tax.

The family formulated goals for themselves:

- Partially repay your monthly mortgage early.

- Save for a vacation trip. Save the amount of 100,000 rubles. To ensure that the amount does not depreciate in six months, convert monthly savings into dollars.

The amount that the family saves for vacation also serves as reserve capital. If there is an emergency with money, it can be used.

| Month | September | October | november | December | January | February |

| Income (thousand rubles) | ||||||

| Salary | 100 | 100 | 100 | 100 | 100 | 100 |

| Prize | — | — | — | 15 | — | — |

| Tax deduction | 10 | 10 | 10 | 10 | 10 | 10 |

| Compensation for kindergarten | 1 | 1 | 1 | 1 | 1 | 1 |

| Total income: | 111 | 111 | 111 | 126 | 111 | 111 |

| Expenses | ||||||

| Mortgage repayment | 25 | 25 | 25 | 25 | 25 | 25 |

| Communal payments | 7 | 7 | 7 | 7 | 7 | 7 |

| Kindergarten | 3 | 3 | 3 | 3 | 3 | 3 |

| Children's mugs | 4 | 4 | 4 | 4 | 4 | 4 |

| Internet, mobile communications | 1 | 1 | 1 | 1 | 1 | 1 |

| Nutrition | 30 | 30 | 30 | 30 | 30 | 30 |

| Household chemicals | 3 | 3 | 3 | 3 | 3 | 3 |

| Cloth | 2 | 2 | 2 | 4 | 2 | 2 |

| Entertainment | 3 | 3 | 3 | 3 | 3 | 3 |

| Present | — | — | 2 | 6 | — | 3 |

| Total expenses: | 78 | 78 | 80 | 86 | 78 | 81 |

| Remainder | 33 | 33 | 31 | 40 | 33 | 30 |

| Early repayment of mortgage | 25 | 25 | 25 | 25 | 25 | 20 |

| Leisure trip | 8 | 8 | 6 | 15 | 8 | 10 |

Following this plan, the mortgage debt in the amount of 145 thousand rubles will be repaid ahead of schedule in six months. An amount of 55 thousand rubles will be accumulated for vacation.

Who needs a financial plan?

All people with a modest income believe that creating a personal financial plan is pointless for them. Practice shows the opposite: the less income, the more a person must control his expenses so as not to go into debt. This is especially true for those who have .

Planning is what will help him not make meaningless spontaneous purchases, and clearly understand how much he can spend per day on groceries or clothes.

A wealthy person controls not his expenses, but his income. He needs to draw up a plan for investing personal income so that income is not only maintained, but also increased.

Every family will benefit from a personal financial plan. Try it now and take control of your budget.

Nina Polonskaya

A personal financial plan is the first step towards achieving your goal and achieving financial independence. The vast majority of rich people have their own financial plan, thanks to which they competently manage their cash flows and, as trite as it may sound, this allows them to become even richer and feel more confident in terms of financial security. A well-drafted plan provides a certain algorithm of sequential actions, the implementation of which will allow you to achieve your intended goal at the lowest cost. Even a simple plan will allow you to feel more stable, get rid of debt, live mediocrely, and ideally significantly improve your financial situation.

Most people don't have a clear financial plan. But nevertheless, they still have some desires. And to the question of what would you like in this life, the answers will be approximately the following:

- a lot of money A LOT OF MONEY;

- apartment;

- cottage or house by the sea;

- do not work and live on interest from capital;

- car;

- to travel a lot;

- pay off debts.

Go ahead. We ask them: “How are you going to achieve this?” And then there comes a long pause. A person begins to scroll through something in his head, think, and comes up with something like this: “Will I earn more in the future?” (we do not take into account winning the lottery and receiving a rich inheritance).

How much more? And when will this happen? And what are you doing for this? And if income increases, what next? How do you want to not work in the future and live entirely on your own funds, which will generate your monthly income? And in general, how much money do you need for this?

And in response there was silence or something completely incomprehensible.

- why do you need a financial plan and what does it provide;

- how to correctly formulate your goals;

- complete compilation algorithm in 4 steps with examples;

- how to avoid mistakes and increase the efficiency of achieving your goal.

The article turned out to be quite lengthy. But I tried to take everything into account in it. After reading it you will receive complete information on the correct preparation of your plan.

Why do you need a financial plan?

What is a personal financial plan (LPP)? This is a kind of map, a kind of guide that helps you move towards your goals along the right path, with the least obstacles and difficulties, taking into account all the nuances. If we compare it with other areas in life, we can draw an analogy. Let's say you travel to Altai on your own by car. In order to get to a place safely, you need to know: the road map, the distance and, accordingly, how much money is needed for fuel, travel time, associated expenses (food, overnight stays, etc.), things that are needed for the trip. Having such knowledge, you can easily reach the intended point, with maximum comfort. The absence of one of these points in the plan can cause serious obstacles, up to the inability to get to the place (it’s commonplace to run out of money on the road).

Drawing up a plan will take you no more than an hour, well, maybe 2-3 hours if it is serious enough. But the time spent will allow you to clearly formulate your goal and, most importantly, understand how you can achieve it.

People who have a clearly defined financial plan achieve their goals many times faster than those who do not.

Stages of drawing up a financial plan

Where to start compiling LFP? Formation of the plan consists of several successive stages.

Stage 1. Setting goals

Drawing up a financial plan should always start with defining your goals. That is, what you want to achieve. Goals can be long-term or short-term. Not important, important and very important or global. In addition, goals should be specific and better expressed in monetary terms. For example, I want a new car, an apartment, or save up for a vacation - on the one hand, these are goals, but on the other hand, they carry absolutely no information. It would be more correct to formulate this way - I want:

- a new BMW car for $30,000;

- 3-room apartment in the center of your city for 5 million rubles;

- save 100,000 rubles for vacation.

So we have specific goals. And now it becomes more clear how much money is needed to achieve them.

Stage 2. Timeframe for achievement

The goals have been set. Now you need to determine the time during which you plan to achieve them. When there are no exact deadlines, the goal becomes something illusory and distant. Specifically, using the above examples, you can do this:

- buy BMW in 3 years;

- apartment in 10 years;

- vacation - accumulate by May next year.

Deadlines and goals need to be set realistically, based on your financial capabilities. The dream of having a million dollar house and several million dollars in your account is certainly good. But if you receive the average salary in the country, then your plan is doomed to failure from the very beginning. As well as the goal of saving up for an apartment worth 100 thousand dollars in 2 years with a salary of 1 thousand dollars. Be realistic.

Stage 3. Assets and liabilities

This is the most important point. Moreover, compiling it will take the lion’s share of time. And success in achieving your goals depends 90% on him.

You need to determine for yourself how much money you can save monthly. First you need to determine the size of assets and liabilities in your budget. That is, how much you receive and spend. The difference will be the amount that can be allocated.

Assets are what bring you money or your income.

Liabilities - they take money, that is, your expenses.

We draw up a table of assets and liabilities.

It is not necessary to know every expense item down to the last penny. You can initially generate data approximately “by eye”. The most important thing here is to see the overall picture of your income and expenses and in what proportion this or that expense item accounts for the total amount.

| Assets | Income | Liabilities | Expenses |

| Salary | 50 000 | Loans | 8 000 |

| Interest on deposits | 5 000 | Communal payments | 5 000 |

| Renting an apartment | 10 000 | Nutrition | 15 000 |

| Dividends on shares | 5 000 | Cloth | 15 000 |

| Part time job | 10 000 | Directions | 3 000 |

| Household expenses | 3 000 | ||

| Entertainment and relaxation | 20 000 | ||

| Sport | 2 000 | ||

| TOTAL: | 80 000 | 71 000 |

The table shows that the net balance each month is 9,000 rubles. Based on this, you need to adjust your goals and deadlines for achieving them.

It was more logical, of course, to start from this stage, and then move on to setting deadlines. But I advise you to do it in this order. Why? If you immediately determined how much money you have left and the period until you achieve the plan based on these plans, then you would end there. The discrepancy between the desired and actual deadlines gives you an incentive to look for ways to fix it.

Stage 4. Invest money

After determining the goals, deadlines and the amount that you can save monthly according to your personal financial plan, you need to make sure that the money does not lie as a dead weight, but brings additional income. Depending on your goals and time frame, you can use different financial instruments to make a profit. The following rule applies here: the longer the period of achieving your goals, the more risky and profitable instruments you need to invest money in.

A few examples.

- Money for vacation in 1 year. At the appointed time, you must have a certain amount that will be enough for the trip and related expenses. And here the most important thing for you is stability and security. Therefore, the best option is bank deposits with their almost 100% reliability. If you are planning a trip abroad, it is advisable to additionally open a foreign currency deposit. This way you will protect yourself from sudden sharp jumps in the dollar (euro), when money accumulated in rubles can sharply depreciate.

- You are saving for your child's education. The money will be needed in about 8 years. The term is quite long, so bank deposits, with their low interest rates, are not the best option. Investments in bonds and stocks, whose potential income is 1.5-2 times higher, are most suitable for you. 1-2 years before the target date, gradually transfer money to more conservative instruments to avoid unpleasant situations in the form of drawdowns in shares. Here again we turn our attention to bank deposits and government bonds with their highest degree of reliability (OFZ).

When drawing up personal financial plans, many people make the same mistakes and do not take into account many factors. This together makes it difficult to achieve the intended goals, and in some cases makes them impossible. It is better to know all the pitfalls right away on the shore and swim with the flow, and not against it. Additionally, our advice can significantly speed up your process, in some cases even significantly.

Unrealistic deadlines and amount of goals

As already described above, there is no need to wish for yourself what you are unlikely to achieve. It's better to focus on more real things. Of course, the goal may be slightly too high. This will give you an incentive to look for additional opportunities to make your dream come true.

Too much amount

This refers to the amount set aside monthly. Of course, the more you can save the better. But you don’t need to tighten your belts to the limit and live on 5 kopecks a week. The goal is of course good, but you need to live now. Moreover, constantly living in spartan conditions, you risk one day giving up on everything, all your goals and plans. Therefore, leave yourself some financial reserve to breathe more freely.

Lack of discipline

Setting goals and making a plan is only half the battle. You could even say this is the simplest and easiest thing. What awaits you ahead will be a real test for you. You can create a plan in just an hour, but you need to stick to it for several months (years, decades). The success of your venture will depend on your actions in the future.

Too long

It is very difficult to stay motivated and stick to a month-to-month plan that spans several years. Therefore, further break it down into several stages. It will be much easier to reach everyone. And the motivation will be at the level. If you are saving for an apartment (country house) for 10 years, then the 1st stage will accumulate 10% of the cost within a year. You can take into account the footage of your future home - save for the kitchen, hallway, bathroom, toilet. Then, for example, the accumulated money would be enough for you to buy out 1 room, then another. Think of something similar for yourself.

Inflation

For some reason, almost everyone forgets when money depreciates. This is especially true over long periods of time. Agree that 10,000 rubles now and 10-15 years ago are two big differences. Previously, you could buy a lot more with them. The same goes for your plans. If you plan to save a certain amount, it may turn out that by the original date it will not be enough due to the fact that during this time the prices for everything have increased. But here they will come to your aid...

Compound interest

They work in conjunction with inflation. Typically, the higher the inflation rate in a country, the higher the return on investment will be. But here it is the difference between income and current inflation that needs to be taken into account. It is this difference that will show your real income.

By investing money at 15% per annum with annual inflation in the country at 10%, your real income will be 5% per annum.

How to find out this profitability? It is very difficult to determine the exact figure. But there is a certain average interval:

- Bank deposits - real yield 0 - 3% per annum

- Bonds - 2-5% per annum

- Shares - 3-8% per annum.

Pay yourself

After receiving income (salary, bonuses), we immediately set aside a predetermined portion for your goals. This will relieve you of the constant headache of where to get money at the end of the month, when almost everything has already been spent, but nothing has been put aside yet. Additionally, you will not be tempted to spend this money on other “necessities.”

Exact adherence to plan

On the one hand, this is good, but there is no need to blindly carry out everything planned in advance and fully automatically. You can make small adjustments based on your current capabilities. We raised your salary, gave you a good bonus, found a part-time job - we adjust the plan. Such periodic review can give you a significant acceleration in moving towards your goal. There are many options: save everything you receive above the average salary: either it’s all, or half, and spend the other half on yourself for your loved one, or save a certain percentage of what came from above, or a fixed percentage of your entire income. We received a lot - we put a lot aside, our salary was cut - we reduce the contribution to the dream in the same proportion.

Optimization of expenses and income

The easiest way to achieve your financial plan faster is to save as much as possible. How to do it? There are only two ways - we reduce expenses and increase income. The easiest way to start is by optimizing your costs. Once again, carefully analyze what can be reduced and what can be completely abandoned in the name of a good goal. Perhaps you spend too much on entertainment, alcohol, smoking, lunches in cafes and restaurants. Everyone can find something of their own that they can limit themselves to (a little or completely).

After such optimizations, you can save significantly more money, which will ultimately give you the opportunity to achieve your goal much faster. Or get a more significant financial result within a predetermined period. What to focus on? Almost any family can save an additional 10 to 30% through small optimizations.

By investing 3,000 rubles in the stock market every month with an average annual return of 15%, after 15 years you will have 2 million rubles in your account. But if you increase the contribution amount to 5 thousand, you will receive an additional 800 thousand!

If you save 10% of your income, but then were able to optimize your expenses by 20%, then the amount of free funds you have will triple and things will go 3 times faster.

Where to keep records?

Is accounting necessary at all? Or can you just save money and not think about anything? In principle, this option is also possible. If you have an iron will, determination, excellent memory and your goals are not too long-term. But why all this? It’s easier to keep records, recording your achievements and the stage at which you are now and how much time you still have left until the end of the journey (time and money).

There are several accounting options. You can keep a notebook, a kind of income and expense book, and make notes there. The second option is to record everything on your computer in an office program, such as Excel. Once you have set up and entered the necessary items of expenses and income, as well as your goals, all you have to do is enter the numbers in the appropriate columns. You can even download a sample financial plan in a ready-made Excel spreadsheet and modify it a little to suit yourself.

But I think this is a long-outdated option. We live in the era of computer technology and a fairly large number of programs have already been created that significantly simplify the maintenance of such accounting and, in particular, the achievement of a personal financial plan. The only negative is the likelihood that such a service will be closed by the developer. Your Excel tables will not go away, but data on a third-party service may be lost forever.

Therefore, here you need to choose the right service that has been working for several years. Personally, I have been using the free EasyFinance.ru program for several years.

There are a lot of advantages. Simpler accounting, the ability to easily access your data in the past, with the preparation of various reports: how much you received previously, how much you spent, saved, what share of a particular item of expenses-income from the total, what stage of the financial plan you are at and how much you left. You can maintain several plans at once. All this can be done with just one click of the mouse. And what I especially like is the ability to build all kinds of graphs, charts and interesting reports. This would be difficult to achieve in Excel.

How is there no such specific deadline? For minor goals, such as buying a new computer, phone, saving for repairs, it is recommended to draw up a plan for six months to a year. If your goals are more global, buying an apartment, saving for old age, then make a plan for several years in advance. This could be 10, 15 or 20 years. Further, it is advisable to break this period into several smaller ones. Nobody knows what will happen to you and your income in a few years. Therefore, we will definitely formulate a first plan for the next 2-3 years, and then based on your capabilities.

Is it possible to have several LFNs?

Of course you can. In this case, you need to choose priority ones among them, determine in what proportion you will contribute funds to achieve each goal. Of course, you need to save more for more important goals. But it is advisable to have no more than 2-3 goals. Otherwise, you risk wasting all your money on them and ultimately not achieving a single goal.

I have an existing loan, does it make sense to make a plan or is it better to pay off my debts first?

Repaying a loan ahead of schedule is also a kind of financial plan. But if you have other goals in your plans besides repayment, then 2 options are possible. If you have a very expensive loan (20-30% per annum), then of course it is better to first throw all your energy and resources into repaying it. And only then begin to formulate your plans for the future. Otherwise, you will always be at a disadvantage. We invested the deferred money at 15% per annum, and the loan costs were 2 times higher.

If you have free debts (borrowed from friends, acquaintances), give some of them to pay off, and use the other part for your plans.

A mortgage loan taken for many years stands apart. Here, too, you need to approach it based on logic and your capabilities. Either pay it off as soon as possible, thereby saving a significant part of the funds from the loan, or accept everything as is and, in addition to monthly loan payments, simultaneously implement your other financial plans.

Drawing up a financial plan using an example

Based on all of the above, all the recommendations and advice, let's look at an example of how to correctly draw up a financial plan, optimize it and implement it.

Ivanov Ivan Ivanovich wants to accumulate capital, which will allow him to leave his job and live in the future on interest. His demands are not too great and 30 thousand rubles a month is enough for him.

Forming a goal. 30 thousand per month is 360 thousand per year. We need to determine the amount of capital to own and ensure a given return.

There is a simple rule of two hundred. This means that the monthly profit must be multiplied by 200. Why 200? This corresponds to a conservative yield of 6% per annum, but with almost 100% safety of funds.

In our case we get:

30,000 rubles / month x 200 = 6,000,000 rubles

There is a goal: 6 million rubles

Now we evaluate the current financial position, that is, assets and liabilities. Let's make a table.

Income exceeds expenses by 5 thousand rubles. This is exactly the amount that can be saved monthly. But with such deductions, you will need to save for 100 years. And Ivanov would like to keep it within 10 years, maximum 15.

This means you need to increase the size of your monthly deposits. We will cut costs. Let's see what we can sacrifice. You need to start with the largest articles so that optimization gives greater results.

As a result, it was decided:

- Quitting smoking saves 3,000 rubles.

- Reduce expenses on alcohol - 500 rubles.

- Reduce trips to the cafe at work - 2,000 rubles.

- Buy food and clothes more thoughtfully and in advantageous places - an additional minus 3 thousand.

- Recreation and entertainment have also been slightly reduced - the winnings are 500 rubles.

As a result, every month an additional 9,000 rubles will remain. Total: you can safely save 14,000 rubles a month. This is about 30% of total income.

In addition, sometimes Ivanov is given additional bonuses at work. Plus it happens to earn money on the side. According to a rough estimate, this brings in about 100 thousand a year. On average 8 thousand per month. Ivanov decides to spend some of this money on himself, and 5 thousand will go into the piggy bank.

Total: you can save 19 thousand a month with virtually no damage to your budget.

Now we determine where we will invest the money. Since the goal is quite serious and the implementation of such a financial plan will take more than one year, the most optimal would be to invest money in the stock market, namely in.

Investing in stocks is considered a risky investment, but has the potential for high returns. You can reduce risks without loss of profitability by increasing the investment period.

Taking into account inflation and projected long-term profits, we have a real return of 6%. Using a calculator, we calculate how much time we need to earn 6 million. (It would be more correct to say - an amount equivalent to today’s 6 million, for which it would be possible to buy the same amount of goods and services as now with this money).

The period is about 15 years. This is exactly the time you need to fulfill your financial plan.

On the one hand, the period is quite long. But Ivanov has 4 options for the outcome of events:

- He will achieve his goal exactly on time.

- Will arrive ahead of time.

- By the appointed time, he will not have time to complete everything planned. But he will already have some capital.

- He will spit on everything and spend all the money.

As you can see, 3 out of 4 outcome options are positive. That is, the chance of achieving certain success is quite high.

If you do something, then you have two possible outcomes: it will work out or it won’t work out. If you do nothing, then you only have one left.

1. Spam. All investors are annoyed by messages that invite them to “call to learn about the most disruptive technology since the invention of the wheel.” You can be sure that even if he then receives your business plan, he will put it at the bottom of the pile. Asking an investor to look at and comment on your site is just as bad.

2. Business plan without a resume. Summary–

This is a one-page “elevator speech” (and can be presented separately from the business plan) that gives the investor a complete overview of the key parameters of the business. Many business plans do not have a normal summary, or vice versa–

a business plan looks like an extended resume. Both options are bad.

3. Lack of plan in the business plan. Many business plans that are sent to investors are actually extended product specifications that give more than enough information about the product and nothing about how and where you plan to sell it and make money.

4. Illiteracy. Blots, typos, grammatical and spelling errors, handwritten documents will only convince the investor that you will also conduct your business unprofessionally. Keep in mind that investors invest in people first and foremost, and then–

into ideas.

5. Overfilling the text with abbreviations. Don't forget that the people who will read your business plan, while not stupid, will not be aware of the terms or acronyms used in your industry. They will consider the heavy use of abbreviations to be a result of inattention, laziness, or perhaps deliberate confusion of the reader. Try to stick to commonly used vocabulary.

6. A book instead of a business plan. Don’t be too verbose, don’t fill your business plan with unnecessary information. A business plan for an investor should be no longer than 30 pages. Stick to the facts, state them clearly, and don't repeat yourself unnecessarily. Planning too long-term will create the impression that your business is too complex and risky.

7. Links to applications. Investors do not object to documents supporting the basic business plan. But it must impress and be complete without applications. The thickness of a business plan or the presence of dozens of applications is not impressive in itself.

8. Negative statements. Don't say anything about your competitors or clients that you couldn't prove in front of them. Many business plans contain claims like “poor usability,” “low quality,” “big and cumbersome,” all without any justification. Investors view such statements as signs of unprofessionalism and a lack of ethics unless they are supported by third party data.

9. Prototypes and demo versions. Don't forget that at an early stage, prototypes tend to break, and demo versions hang or don't work in unfamiliar hands. Therefore, they cannot adequately reflect all the work and passion you put into them. Pictures and words will make a much better impression.

10. Letters from your partners. Letters of recommendation from an investor's partners will be helpful, but letters from your partners will not carry the same weight. But the presence of reviews from clients and suppliers and concluded contracts will make the right impression.

Personal financial plan is the basis for the financial well-being of you and your family.

Many people dream of a new car, apartment, country house, passive income in retirement or other things. But unfortunately, most of these desires remain just dreams and are never realized or only partially realized. The reason is the lack of a financial plan.

What is a personal financial plan?

A personal financial plan is an action plan for achieving financial goals and solving financial problems.

With the help of a personal financial plan, you will be able to manage your money wisely, see a picture of your financial future, increase your income and investment efficiency.

You will be able to assess how feasible your goals are and what needs to be done in the current situation to achieve them in the optimal time frame. The plan allows you to calculate how certain financial decisions will affect the life of the family.

Why do you need a personal financial plan?

With the help of LFP you can:

- assess your current financial situation;

- optimize personal finances and assets;

- create financial protection and reduce risks;

- achieve your desired financial goals in the most optimal way;

- determine a plan of action, thereby avoiding rash decisions;

- create capital to purchase real estate or pay for education;

- provide for old age.

The mistake many people make is that they start thinking about their goals too late. For example, they remember that they need an increase in their pension 5-10 years before retirement, that their children need to pay for university education for 1-2 years, and so on. The sooner you think about your financial future and take action, the easier it will be to ensure your financial well-being.

- A personal financial plan will help you plan to achieve your financial goals;

- Optimizes your finances and helps you find hidden financial reserves;

- Will answer the question whether your goals are achievable in your current financial situation;

- Will tell you what needs to be done to achieve your goals on time;

- Build a graph of your cash flows and capital growth;

- Calculate what amounts need to be invested and how much you will have accumulated by the end of the term;

- Shows a financial picture of your future.

For what purposes can you create a financial plan?

A personal financial plan can be created for different purposes. The most popular financial goals:

- Financial independence;

- Providing a pension;

- Apartment, house or cottage;

- Real estate abroad;

- Teaching a child or your own training;

- Trips;

- Wedding and birth of a child;

- Car;

- Own business.

For what period is a financial plan drawn up?

LFP can be drawn up for any period - from one year to the end of life. It is recommended to review the plan at least once a year, since changes in life situation may require adjustments to the plan.

What is involved in creating a personal financial plan?

The financial plan is drawn up based on the data of the client and his family and includes several stages of work:

- Data collection. Initial consultation by phone or Skype and questionnaire. At the first stage, you need to fill out a form in which you provide the information necessary for drawing up the physical form:

- list of financial goals (timing and cost);

- current income/expenses;

- list of assets and liabilities;

- risk profile (determined using a questionnaire).

- Diagnostics. This is an assessment and analysis of the client’s current financial situation. At this stage the following will be produced:

- analysis of income and expenses, cash flow, assets and liabilities;

- calculation of investment potential was made;

- recommendations were given for optimizing assets and liabilities, income and expenses.

- Financial protection. Includes analysis of current financial protection and possible risks. Recommendations will be made to create or improve financial protection. A selection of the necessary tools to create financial protection has been made.

- Pension provision. The client's current pension decisions will be analyzed and recommendations will be given on increasing pensions and creating pension benefits.

- Tax planning. Searching for ways and recommendations to optimize and reduce the client’s tax burden.

- Analysis of financial goals. At this stage, financial goals are prioritized and scheduled, as well as an analysis of their achievability.

- Investment strategy development and portfolio construction. This stage includes:

- development of an investment strategy to achieve the goals set by the client;

- selection of a company for investment (brokers, banks, insurance companies);

- compiling an investment portfolio and selecting financial instruments;

- detailed description of the selected instruments (composition, commissions, prices, etc.);

- calculation of portfolio profitability and risk indicators;

- recommendations and rules for investment portfolio management;

- warning about the risks associated with investing.

- Calculations. Financial plan calculations. Demonstration of the dynamics of cash flows and capital in graphical and tabular form.

- You receive a developed financial plan in the form of a report and attached documents.

Order completion time: up to 6 weeks.

Service cost: 30,000 rubles.

Financial plan support

The financial plan must be regularly monitored and revised if necessary. Personal circumstances change (income, expenses, life priorities and goals), legislation changes, new opportunities and financial instruments appear. All this affects the achievement of your goals. Also, in the process of implementing a financial plan, many questions arise, and sometimes difficulties that require the help of a consultant.

All this cannot be foreseen in advance. Therefore, for a financial plan it is recommended to order annual support. If accompanied, you will have the opportunity to monitor and adjust the implementation of your financial plan together with a consultant, as well as receive advice on issues that interest you regarding your plan and personal finances.

To attract and invest funds in any business, an investor needs to carefully study the foreign and domestic markets.

Based on the data obtained, draw up a project estimate, an investment plan, forecast revenue, and generate a cash flow report. All the necessary information can be most fully presented in the form of a financial model.

Financial model of an investment project in Excel

Compiled for the projected payback period.

Main components:

- description of the macroeconomic environment (inflation rates, interest on taxes and fees, required rate of return);

- projected sales volume;

- projected costs for attracting and training personnel, renting space, purchasing raw materials, etc.;

- analysis of working capital, assets and fixed assets;

- sources of financing;

- risk analysis;

- forecast reports (payback, liquidity, solvency, financial stability, etc.).

For a project to be credible, all data must be confirmed. If an enterprise has several income items, then the forecast is prepared separately for each.

A financial model is a plan for reducing risks when investing. Detail and realism are a must. When drawing up a project in Microsoft Excel, follow the following rules:

- initial data, calculations and results are on different sheets;

- the calculation structure is logical and “transparent” (no hidden formulas, cells, cyclic links, limited number of array names);

- the columns correspond to each other;

- in one line – formulas of the same type.

Calculation of the economic efficiency of an investment project in Excel

To assess the effectiveness of investments, two groups of methods are used:

- statistical (PP, ARR);

- dynamic (NPV, IRR, PI, DPP).

Payback period:

The PP coefficient (payback period) shows the time period during which the initial investment in the project will pay off (when the invested money is returned).

Economic formula for calculating the payback period:

where IC is the investor’s initial investment (all costs),

CF – cash flow, or net profit (for a certain period).

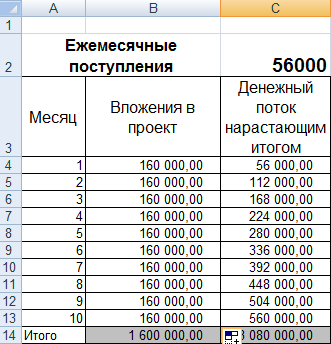

Calculation of the return on investment project in Excel:

Since we have a discrete period, the payback period will be 3 months.

This formula allows you to quickly find the payback period of a project. But it is extremely difficult to use, because... monthly cash receipts in real life are rarely equal amounts. Moreover, inflation is not taken into account. Therefore, the indicator is used in conjunction with other performance assessment criteria.

Return on Investment

ARR, ROI – profitability ratios showing the profitability of the project without discounting.

Calculation formula:

where CFav. – average net profit for a certain period;